Apar Industries

A MNC operating in Power Transmission, Petrochemical and Telecom sector

Hi fellow investor,

( Disclosure: I own shares of Apar Industries Ltd and hence my views on the topic is biased. Everything I conclude in the article is solely my opinion based on publicly available information. This should not be taken as financial advice. This is purely for educational purpose.)

Let’s get straight into it.

First a little History on the company!

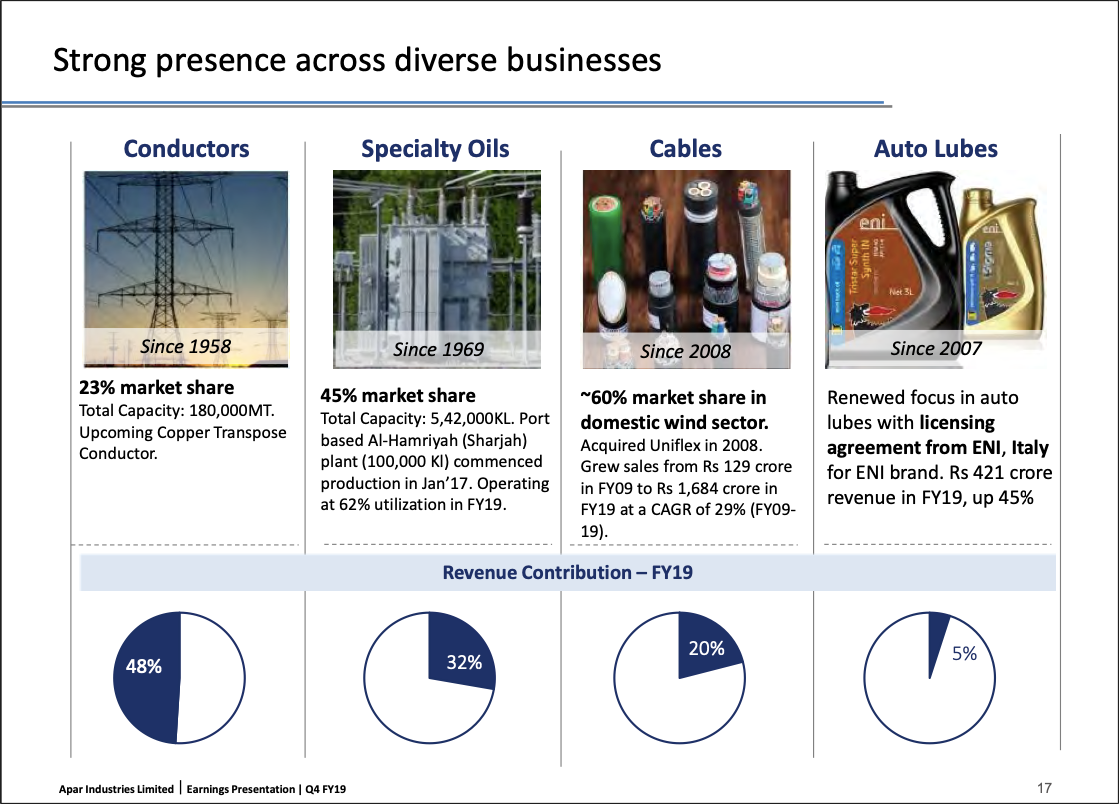

Apar Industries was founded by late Shri. Dharmsinh D. Desai in 1958 as a manufacturer of power transmission conductors. It soon diversified its business into speciality oils in 1969 with a Special Oil Refinery in Mahul, Chembur. It has since grown these businesses multifold becoming one of the largest producers of conductors in the world with a total capacity on 180,000 metric tons and the fourth largest manufacturer of transformer oil in the world with total capacity of 542,000 Kilo-litres. In 2008, the company acquired Uniflex Cables, a manufacturer of cables for power and telecom sectors with an annual turnover of around Rs. 1800 million, for a consideration of around Rs 1300 million.

The company today in managed by Kushal N Desai ( MD and Chairman) and his brother Chaitanya N Desai ( MD). They are the promoters of the firm, holding 59.69% of the Total Shares Outstanding (as of June 2020).

Performance over the last decade -

The company has grown the Consolidated Revenues from Rs 23,500 mil in FY10 to Rs. 74,600 mil in FY20 (CAGR = 12.2%), while the EPS in the same time has gone from Rs 8 per share to Rs 35 per share (CAGR = 15.9%). The company benefited greatly in the second half of the last decade from the increased investment of the Indian government on Infrastructure especially Rural Electrification. The company is heavily dependent on infrastructure spends in the Power sector, getting around 80% of its Revenue from the Power Sector. The company has a diversified Revenue base but it also means that they are exposed to wide variety of commodity price fluctuations. The fall in the price of commodities has to be passed on to the customers and when they fall abruptly the company has to take a loss on their existing inventory, this along with the intense competition in the domestic and international markets have squeezed the margins and has impacted their profitability over the last few years, despite the increase in the top line performance.

To counter this the company has spent close to Rs 7000 mil over the last five years, on higher value added products and de-bottlenecking existing capacity to reduce costs. The company has funded this capex through a mix of internal accruals and debt, and has still managed to bring down the debt over the last decade from Rs 6000mil to Rs 3460 mil (as on June 2020). Due nature of the industry, the company requires large amount of capital in the short run to import the raw materials (which form more than 80% of their costs) and as their customers generally require longer credit terms, the company thus uses ‘letter of credits’ (or LoCs) to import raw materials. This is an added cost for the company as the LoCs are interest free for 35-45 days only but since on the customer side the debtor days are around 90, Apar pays an interest for the remaining days. This is one of the reasons why despite lowering the Debt on the balance sheet, the finance cost for the company has increased. As of June 2020 the company has Rs 14650 mil of LoCs on its book. Though the interest cost has increased in absolute terms, as a percentage of Revenue, they have remained around 3% mark for the last ten years. The interest costs also include the forward cover costs (the company hedges its forex exposure through forward contracts).

Conductors-

The conductor business is the largest segment for Apar, it contributed around 48.6% of the total consolidated revenue in FY20. The company setup its first conductor plant in Silvassa in 2002 and has since expanded the capacity there to about 83,000 Mt, in addition to that they setup new plants in Athola (46,000 Mt) in 2014 and Jharsuguda (30,000 Mt) in 2017. The company has also expanded their product portfolio by spending on R&D as well as through licensing agreements. In 2013, they signed an agreement with CTC Global, USA to manufacture their patented High Temperature Conductors called ACCC under CTC’s license. They have since added High-efficiency conductors (HEC), Copper Conductors (for Railways) and Copper Transpose conductors (CTC) to their product portfolio.

These value added products have higher margins and lesser competition than the conventional conductors that the company supplies. While the conventional conductor business has become highly commoditised and the advantage for a company like Apar comes from its size and ability to reduce the cost of production, with minimal room to do so. The higher value added products though have a higher barrier of entry due to the large initial capex required and then the longer gestation period to get the products approved from the clients. The demand for these high value products are increasing, currently these products contribute 38% ( 18% for HEC alone) of the total revenue from Conductors segment, though the effect is limited on the bottom line.

The EBIT margin line is quite up and down over the last ten years, few reasons for it-

It is cyclical industry as the revenue depends on the power infrastructure spends and the power infra spends are increasing but they are lumpy.

The margins depend heavily on the commodity prices, and large swings in these prices affect margins, especially in the domestic market where the orders have moved to Tariff based Competitive Bidding (or TBCB). There is intense competition with competitors bidding prices lower and increasing risk of loss , if raw material prices change.

Company has been consistently spending on expanding capacity and on new products. They have spent close to Rs. 5000 mil in the conductor segment in the last ten yrs ( FY11 to FY20).

To counter the raw material price fluctuations the company hedges Aluminium LME, but it has no way of hedging steel prices. The EBITDA per tn for the segment over the last ten years has fluctuated widely with changing commodity prices (esp. aluminium & steel prices), though the management has indicated their aim to maintain it around Rs 10,000 per tn.

They intend to stabilise margins by reducing conventional conductor orders to 50% of Revenue ( rest hence coming from value added products) and letting go off low margin orders and more importantly focusing on the export market. Exports accounted for 40% of the conductor revenues in FY20, and company aims to increase it beyond 50% in FY21. This would be a prudent strategy as the management has indicated that debtor days is lower for export orders and it also offers a natural hedge for its dollar imports. The company though is not free of competition in the export market with Chinese exporters having an advantage over Indian companies, as China has treaties with countries like Australia, giving the Chinese a leg up in prices. The recent China +1 strategy that companies are adopting may come as a benefit to Apar but it is too early to say what difference it will actually make.

Future Demand Scenario-

Copper Conductors for railways- The government plans 100% electrification of railway network , which is 64,600 rkm, off which 39,866 rkm has been electrified. The initial plan was to complete this by 2020, but now the new target is 2024. The annual demand though will depend on the amount of work sanctioned by the Railways but the company looks well positioned to benefit from this.

Further the government has been focussing on reducing the AT&C losses and upgrading the current power transmission network, which will also increase demand for Apar’s higher value added conductors , especially the High Temperature Low Sag conductors.

The increased investment in renewable energy will also lead to corresponding increase in T&D lines and related infrastructure to connect these plants to the grid and so on. The government has an ambitious target of 175 GW of renewable energy by 2022 and 450 GW by 2040. This will require huge spends on transformers and transmission lines which augur well for Apar.

Though Apar is one of the largest players in this segment, it has healthy competition both internationally ( mainly Chinese firms, Midal Cables) and domestically. In India, Sterlite Technology is leading in Optical ground wires ( OPGW) and also present in other conductor segments ( through Sterlite Power) , also Precision wires was first in the CTC segment and is also a leading player in the conductor segment. Other major players include Gupta Power, Hindustan Vidyut and JSK Industries.

Transformer and Speciality Oils-

The transformer and speciality oil segment contributed 31% of the Revenue in FY20. Apar is the fourth largest manufacturer and marketer of transformer oil in the world. The company setup its first speciality oil plant in Rabale in 1998, and has since added plants in Silvassa (in 2000) and most recently in Hamriyah, UAE ( in 2017). Currently the company has a total capacity of 5,42,000 kl. The company also diversified into the Automotive lubricants segment in 2007, by signing a manufacturing license agreement with ENI Spa Italy , to manufacture and distribute their “Agip” brand in India. Apar currently manufactures over 400 different types of speciality oils, under four major categories- Transformer oils, White Oils & Liquid Paraffins, Industrial/ Automotive Oils and Process Oils, and they are all marketed under the ‘Powerful’ brand name. According to the company they have 60% market share in the power transformer oil and 40% market share in the distribution transformer markets.

The revenue in this segment is largely dependent on the prices of crude oil. As seen here-

The margins are dependent on the price of base oils and the product mix for the year. The high voltage power transformer oil, automotive and industrial oils have better margins than the oils used in distribution transformers. Moreover, the base oil prices can’t be hedged and the company has inventory , almost 60 days at all times, thus any major price changes can cause margin losses for the firm. As specified by the management below-

On the debtor side increasing credit terms hurts the company as it will increase the interest cost on the LoCs that the company has taken, hence keeping the cash cycle short is essential.

The automotive and industrial oil segment has done reasonably well for the company, contributing 24% of the sales and 14% of the volumes in Fy20. The management has also indicated automotive and industrial oils offer higher margin than others in the segment.

Although automotive and industrial oils are also affected by the sudden fluctuations in crude prices, as these products have longer supply chain distribution cycle than transformer oils and OEMs pricing are fixed on quarterly basis. Thus even sudden increases in oil prices are shown in the numbers with a lag.

The company has setup a 100,000 kl capacity plant at the Hamriyah FZE , in Sharjah, UAE. Apar has also received the good manufacturing practice license from FDA, for the Hamriyah Plant and should be able to supply to more Pharma and cosmetic companies and increase their naphthenic oil and other high performance based oil business. The company exported approximately 65,000 kl of oil to the MENA region and hence being closer to their customers will give them an advantage over their competitors.

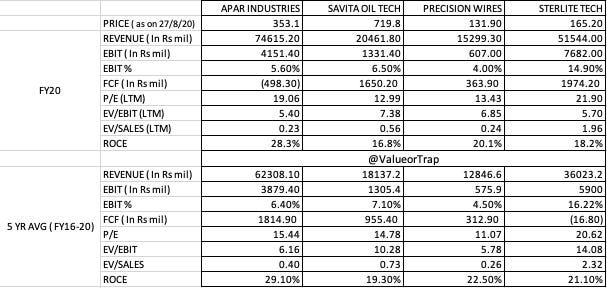

The major competitor for the company is Savita Oil Technologies. They have a similar product portfolio to Apar and are major players in the transformer oil market as well with market share of around 30%. Savita is also a player in the automotive lubricant market, selling under the brand name ‘Savsol’, getting revenue close to Rs. 5500 mil compared to the Rs 5300 mil for Apar, in FY20. Overall both are now of similar sizes but Savita has been more profitable over the last few years. The difference can partly be attributed to the higher depreciation due to commissioning of Hamriyah plant which cost the company over Rs 1000 mil to build.

Future Demand Scenario-

By end of March 2020, India had a total transformation capacity of 971,503 MVA, off which the HVDC capacity was 25,500 MVA. The govt according to their 13th Five year Plan, will add another 38,634 MVA by 2022, off which HVDC capacity would be 5000 MVA. Apar has a high market share in the HVDC segment and should definitely benefit from this demand. With addition of around 68,000 MVA in 2020 alone, this demand alone won’t be sufficient.

The green corridor the government plans to set up with 175GW of Renewable energy and also the further addition in thermal power, will see demand for transformers and hence transformer oil rise. Though all these targets are dependent on the fiscal expenditure of the government, which will be under pressure, after the fall in the tax revenues due to the pandemic. So though this demand may come but it seems it will be later rather than sooner.

Automotive lubricants sale were hit last year due to fall in sales of OEMs, & due to Covid-19, FY21 will be another tough year for auto lubes. Going forward though at least in the medium term the company should be able to grow both the industrial and the automotive lubricant business. The demand disruption due to EVs still seem a fair bit away, but the company may still somewhat benefit from the increase in transformer oil business, as transformers would be required for setting up charging stations across the country.

Cables -

The company has been successful in turning around the Cable division, since acquiring Uniflex Cables in 2008, and then merging that company into Apar in 2012. The company had sales of Rs. 3112.7 million and a net loss of Rs. 282.5 million in FY11. In FY20 the segment reported sales of Rs. 16025.8 million and an OPM of 11.1%. The company had to put in large amount of capital to turn this business around- which included upgrading the existing equipments and technologies for newer products, & expanding the production capacities. The company moved away from telecom cables to power cables and speciality cables. They invested in Electronic beam machines, which could to be used to improve the product mix. The company today has a wide variety of cables with applications in railways, defence, utilities, solar and wind power plants, and telecom as well.

The company has grown the top-line at CAGR of 20.9% since restructuring in 2012 and also improved the profitability significantly.

The government schemes for power transmission, has increased demand for power cables, like HT-LT cables significantly. Company has become the largest supplier of cables to the renewable sector in India. The company has continued to make investment into the cables sector, seeing as it is their fastest growing segment, they have commissioned a a third E-beam machine, at a cost of around Rs 900 million, as the other two are running at full capacity and company’s expects demand from the Railways. Company has entered the railway harness business, earlier they used to just supply the e-beam cables, now they will supply the complete cable harnesses for coaches. Company also entered the solar cable harness business and automotive cables. They have also been the first Indian company to develop Medium Voltage covered Conductor (MVCC) which are power cables for last mile connectivity , and offer a higher degree of safety, especially in congested cities areas and forests. Previously this was being imported from a Raychem (the only other company to make this).

The power cable demand has been hit by completion of government electrification schemes and slower off-takes in telecom and renewable energy sectors. The HT-LT and optic fibres have intense competition affecting prices, due to over capacity in international and domestic markets. The Covid-19 impact has also been severe, delaying payments from solar and EPC players, and delaying tenders and deliveries from the railways. BSNL’s financial problems has also affected the Bharat Net program and reduced demand for telecom cables, while the demand from telcos like Jio and Airtel have always been lumpy. Though ‘Work from Home’ transition may lead to increase in optic fibre cable demand.

Future Demand Scenario-

Once the Railways, starts the tendering process ( halted due to Covid), there should be significant demand for company’s power cables and harness business.

The increasing renewable energy capacity in India and rest of the world, especially solar power plants, should be a boost for Apar in the long run.

Currently about 17% of revenues in Cables segment comes from Exports, with many countries wanting to reduce dependency on China, the company can increase exports in the coming years.

Defense contracts being given indigenously will also open up new opportunities.

The major threat to Apar’s business will be the distress in the power sector especially the Discoms. The government has done a liquidity infusion of Rs 900 billion through PFC & REC, though CRISIL is estimating around Rs 580 billion in cash losses in FY21 for Discoms. Apar isn’t directly linked with Discoms but their clients do work with Discoms and delayed payments to them will eventually hurt Apar as well.

LIBOR has a major effect in terms of financing all the purchases in all 3 segments, and with interest rates falling , expect interest cost for the company to fall as well. However the increased debtor days may have the opposite effect as working capital cycle may increase.

Increasing exports will be a double edged sword for the company - hoping for China plus 1 story to play out in their favour, and even if it does managing working capital cycle as the delivery schedule for exports will be longer even though the debtor days will be lower.

Statistical Comparison of Apar and its peers-

Hi!

If you liked the above article, consider subscribing to my newsletter and following me on twitter. We will be posting one such article every month.

Thanks for reading!!

any idea why the payable days are so high for the company ?

Excellent & detailed observations