Jubilant Pharmova

Part 1- Jubilant Pharmova Ltd, a diversified pharmaceutical company...

Hi fellow investor,

( Disclosure: I own shares of Jubilant Life Science and hence my views on the topic may be biased. Everything I conclude in the article is solely my opinion based on publicly available information. This should not be taken as financial advice. This is purely for educational purpose.)

Let’s get straight into it.

Jubilant Life Sciences is an integrated global pharmaceutical and life science company engaged in various sectors including pharmaceuticals, life science ingredients, branded pharmaceuticals and drug discovery solutions.

It operates these businesses through various subsidiaries, including-

Jubilant Pharma - This acts as their holding company for the whole pharmaceutical business which can be divided further into 3 segments,

Speciality Pharmaceuticals, that includes the Radiopharma business and their allergy therapy products,

CDMO, their contract manufacturing business of sterile injectables and non-sterile products and Active Pharmaceutical ingredients (APIs), and

Generics, that includes manufacturing and sale of Solid dosage formulations including CVS, CNS, GI, anti-inflammatory and anti-allergy categories.

Jubilant Infrastructure - It has a 256 acres chemical plant in Bharuch, Gujarat. It has 2 units, and is the largest producer of Vitamin B3 in India and 2nd largest globally.

Jubilant Biosys - It provides drug discovery services and contract research services in partnership with leading healthcare companies.

Jubilant Life Science NV- supplies bulk chemicals like ethyl acetate and vitamins in Europe.

Jubilant Life Science (USA)- Sales and Distribution of advance intermediates, vitamins, life science chemicals and fine ingredients in North America region.

In FY11 they changed their name from Jubilant Organosys to Jubilant Life Sciences and de-merged the agri and polymer business from the firm into Jubilant Industries, to focus more on speciality chemicals and pharmaceuticals.

Currently the company is looking forward to another de-merger. The company will split into two, one of the listed entities will be the pharmaceutical company ( under Jubilant Pharmova Ltd) including, the radiopharma, CDMO, generics and novel drug discovery and development segments. The other will be the Life Science Ingredient business ( under Jubilant Ingrevia) including, the Speciality Intermediates (i.e Pyridine and derivatives) , the Nutritional products (i.e Vitamin B3 ) and the Life science chemicals business ( i.e Acetyl products).

The pharmaceutical company has been the major contributor and driver of the company’s profitability over the last five or so years and this de-merger should in theory be value accretive for it, while the Life Science Chemical business is a commoditised business with much less stable margins despite the company’s dominant position in this segment. Since the de-merger is just round the corner ( by end of Jan 2021) , it makes sense to look at these as two different entities.

So Part 1 will be looking at the Pharmaceutical side-

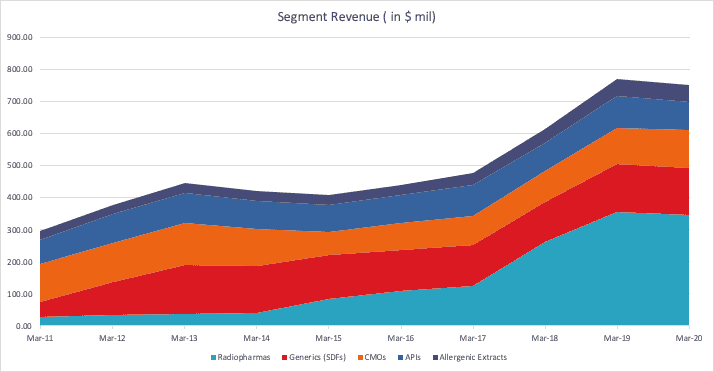

The company has successfully transitioned its pharmaceutical business from a CRAMS (i.e. Contract Research and Manufacturing Service) to a Radiopharmaceutical and Generics manufacturer. The pharmaceutical business has grown at a CAGR of 16% over the last ten years to a revenue of Rs 5975 cr in FY20.

Radiopharmaceuticals- The company entered the radiopharma business in 2009 by acquiring Draxis Pharma for $253 million (around Rs.1000 cr then). Draxis then was involved in radiopharmaceuticals and contract manufacturing of sterile and non-sterile products. The radiopharma revenue has grown at a CAGR of 37% for the last ten years, with the segment contributing around 44% of the Pharma Revenue in FY20, up from around 20% in FY15, and has been the major driver of revenue and profitability growth for the company.

The company is very well positioned in a highly niche segment, manufacturing and distributing diagnostic imaging and therapeutic radiopharmaceutical products. For diagnostics the key products include MAA and DTPA ( in both of which Jubilant has a 100% market share in the United States ). For therapeutics, the key products include Iodine-131 (“I-131”), of which they are one of the only three manufacturers globally. In 2018, in order to further strengthen their position in this industry, Jubilant acquired the radiopharmacy network of Triad Isotopes Inc. for $20.4 million ( approx. Rs. 130 cr then). Jubilant now operates the second largest commercial radiopharmacy network in the United States, with more than 50 radiopharmacies across 22 states.

Jubilant DraxImage’s ( the subsidiary of Jubilant Pharma, that manufactures the nuclear medicines) product offering includes both radioactive products (radio isotopes) and kits (tracer agents) that are paired with the active product for diagnostic imaging procedures. There are two kinds nuclear imaging procedures, SPECT (Single Photon Emission Computed Tomography) and PET ( Positron Emission Tomography). SPECT scans are primarily used to diagnose and track the progression of heart disease, such as blocked coronary arteries, while PET scans is to detect cancer and monitor its progression and response to treatment. SPECT is more widely available and cheaper than PET. PET scans though have superior image quality.

In the SPECT market, Jubilant products include Sodium Iodine-131 solution for thyroid disease and thyroid cancer management, MAA (Macro-Aggregated Albumin) for lung perfusion imaging, DTPA (Diethylene Triamine Penta-acetic Acid) for lung ventilation and renal imaging and MDP (methyl diphosphonate) used in bone scanning. Additionally, they market I-131 Diagnostic Capsules used in thyroid-related treatments, Sestamibi used in myocardial perfusion imaging and DraxImage Exametazime for localisation of intra-abdominal infection and inflammatory bowel disease.

Jubilant brought RUBY-FILL ( a Rubidium Rb 82 generator) to the PET market, after USFDA approval in September 2016, for PET myocardial perfusion imaging (for testing the functioning of heart muscles ). The company claims that, RUBY-FILL offers overall improved diagnostic sensitivity, specificity and accuracy in cardiac PET by enabling improved image quality, higher dosing accuracy and infusion consistency and reliability. Jubilant believes that PET imaging with RUBY-FILL can provide significantly lower patient radiation doses as compared to current SPECT procedures. The cardiovascular PET market is valued at around $62 million ( Annual Report 2018 , pg 12 ). The major competitor for RUBY-FILL would be CardioGen-82 (also a Rubidium Rb 82 Generator) from Bracco Imaging. The two companies ( Jubilant & Bracco) have been locked in litigation since March 2018, with Bracco alleging patent infringement. Jubilant believes these lawsuits are a way to delay hospitals from buying their product in 2018 when some of the Cardiogen-82 supply contracts were going to expire.

The recent Trade Commission and US Patent Office rulings have been in Jubilant’s favour, declaring Bracco’s patents invalid.

Coming to the SPECT side, Jubilant has two major diagnostics products MAA and DTPA, used for lung and kidney scans respectively. The company hiked the prices for these drugs in 2014, MAA vial prices went from $20-$30 to $350-$450 and DTPA increased from $20-$30 to $130-$160 , depending on the quantities bought. The company justified this increase by citing the need to ensure supply sustainability and reliability, as earlier prices would have forced them out of the market, and that the new prices were in line with other radiopharmaceutical unit doses. The company is in an envious position as its the single source supplier for these products, but this is not unique for the radiopharmaceutical industry. There are other manufacturers of these products, with Mallinckrodt supplying MAA in Europe but no plans to re-enter in the US due to financial viability concerns. The major competition for Jubilant would thus come from alternatives. In the US, DTPA is the preferred agent for ventilation studies but in Europe and Canada, majority of the ventilation studies use “Technegas” , which yet to be approved in the US. The manufacturer of Technegas - Cyclopharm, has submitted its NDA on March, 2020 and are confident of attaining approval in 12 month’s time. Cyclopharm estimates the market of pulmonary embolism diagnostics to be worth $90 million in annual sales and hopes to attain 50% market share in three years, rising to over 80% in seven years’ time. Jubilant and Cyclopharm were in advance negotiations for an “exclusive licensing agreement” for “Technegas” but were unable to reach an agreement due to certain license terms.

Jubilant DraxImage (JDI) entered into 43 long term contracts in the US for JDI to supply the distribution networks ( which included radiopharmacies and hospitals) with products for diagnostic and therapeutic procedures. Pursuant to the contracts, JDI will supply the agreed products over a period of 39 months effective from January 2017.

Jubilant’s purchase of Triad Isotope’s radiopharmacy business further strengthened their position in the industry, or at the very least brought them in line with some of their bigger competitors, Cardinal Health and GE Healthcare, both which have have competing products to Jubilant’s and also maintain large radiopharmacy networks- GE maintains 31 radiopharmacies in the US while Cardinal maintains 131 radiopharmacies. The company believes the radiopharmacy network will help increase the sales of RUBY-FILL , due to their sales force and direct contracts with institutional customers.

Though this acquisition, along with the long term contracts have put Jubilant in the limelight. An antitrust class action lawsuit was filed in 2019 on behalf of nuclear pharmacy Ionsouth-Mobile, LLC against Jubilant DraxImage alleging it entered unlawful agreements and monopolised markets. UPPI LLC, the largest association of independent and institutional nuclear pharmacies in the United States, joined as co-plaintiff. They alleged Jubilant entered into anti-competitive behaviour by buying approved NDAs for competing products for MAA and DTPA and “warehousing” them and further increasing prices of these products. They also said - “Beginning in 2017, JDI initiated additional anticompetitive practices, including tying obligations whereby a nuclear pharmacy’s purchase of certain JDI radiopharmaceutical products is conditioned on the pharmacy also purchasing minimum amounts of other JDI radiopharmaceuticals” . Thus forcing pharmacies to pay higher prices and limiting their ability to seek lower priced, higher quality alternatives. While the case is still ongoing, recent reports have suggested, that suit is doomed due to “lack of a competitor willing to enter the respective markets”(as reported here ).

JDI has sales concentrated heavily in North America, and with majority of sales coming from a few products, entering of an alternative (like Technegas for DTPA) is a big threat to their business. The company has stated that it has a pipeline of eight products under development with an addressable market of $ 300 million. The company has launched Drax Exametazime in 2019 with market size of $30-$32 million, with one competitor GE’s Ceretec ( innovator drug). DraxImage also has I-131 MIBG injection, in clinical trials, for treatment of neuroblastoma, a rare form of cancer affecting mostly infants and young children, they expect to file by FY22. Jubilant has also entered into an exclusive License and Distribution Agreement for Navidea’s diagnostic imaging agent Tilmanocept (technetium Tc 99m tilmanocept injection) in the United States, Canada, Mexico, and Latin America. The press release stated- “Tilmanocept, which is entering Phase 3 clinical trials for approval by the United States Food and Drug Administration (FDA), will enable Nuclear Medicine departments to visually and quantifiably localise and monitor activated macrophages in patients suspected of having rheumatoid arthritis (RA). In the Unites States over 1.3 million Americans suffer from this disease.”

The radiopharmacy business has contributed to the top line, adding around Rs 1400cr yearly in the last two years. The impact on profitability though hasn’t been the same. Radiopharmacies, though complementary to their existing business, has some different dynamics as well. The radiopharmacy business is about scale and the margins are much thinner than in the manufacturing radiopharmaceuticals. The complexity in the pharmacy business also arises due to the decay in the radioactive isotopes (contained in the radiopharmaceutical products). Tc99m, an isotope used in many of Jubilant’s radiopharma products has a half life of 6 hours. This short half-life presents certain logistical challenges as customers have to be in a certain proximity to the radiopharmacy to use Tc99m product before it decays or expires. Handling, preparation, and storage of radiopharmaceutical agents require specialised training and specially-equipped facilities, resulting in comparatively high fixed and staffing costs as well. PET radiopharmacies need to have access to a cyclotron ( very expensive as well) to produce F-18 Fluorine (half-life 110 minutes) , and the active ingredient needs to be packaged and delivered to the physicians before the expiration of the radioactive agent. Jubilant has acquired 51 SPECT pharmacies and 3 PET manufacturing sites, with 7 cyclotrons (3 operational) from Triad. But the pharmacy business has been unable to breakeven over the last three years, with the loss after tax rising from 58cr at end of March 2018 to 198.4 cr at the end of March 2020. The company had suggested that they have plans in place to breakeven by FY21 , in the the Q4’FY19 call.

But a conversation with an analyst in the recent Q1’FY21 call, seems to suggest that they aren’t so confident of achieving that goal.

The company has planned to do 5 new launches in radiopharma in the next five years. Negotiating with Cyclopharm for a licensing deal for Technegas will be crucial to make up for the possible loss in DTPA revenues. Further, with the contracts expiring in 2020, the pricing and terms in the new contracts will determine the revenue growth in this segment going forward. The company is looking to expand its base outside North America, and launching RUBY-FILL in Europe will be a help in diversifying revenue through geographical expansion.

Jubilant had shifted most of the assets of their pharmaceutical segment to Jubilant Pharma by 2015. The company supplies their products and services to customers in over 85 countries but still the majority of their customers are based in North America and hence it accounted for over 80% of their Pharmaceutical Revenue. Hence, it makes sense to look at their Revenues in US$ rather than Indian rupees.

While the above chart does show a decent growth in revenue, over the last ten years, that growth is almost solely attributed to the radiopharma segment. Generics, APIs and CMO have been largely flat or even de-grown in the last few years, as seen in the table below.

Generics ( Solid Dosage Formulations) - The company primarily focusses on the manufacture and sale of solid dosage formulations for CVS, CNS, GI and anti-allergy therapeutic categories. As of 31st March 2020, they had 56 products commercialised including 32 in the US, 15 in Canada, 29 in Europe and 29 in Rest of the world ( for comparison they had 46 commercialised products by March 2014- 20 in NAMR, 26 in Europe and 23 in RoW). The Generics contributed Rs 1129.8 cr in revenues in FY20, i.e. 20% of the total Pharmaceutical revenue.

Within the United States, Jubilant says they are market leaders based on market share for several key products, namely, prochlorperazine (largest market share at approximately 52.0%), terazosin (largest market share at approximately 51.9%), methylprednisolone (largest market share at approximately 38.0%), prednisone (third largest market share at approximately 9.0%), olanzapine ODT (second largest market share at approximately 22.0%), donepezil (fourth largest market share at approximately 8.0%), and pantoprazole (fourth largest market share at approximately 13.0%). While in Europe, company prepares dossiers for its product in accordance with the regulations, most of which include their APIs, which they license to European generic pharmaceutical companies in addition to selling their own products in selective countries within the European Union.

Jubilant bought a majority stake ( 82.5% stake) in Cadista Holding in 2005, a generic pharmaceutical company for around $30 million, before buying out the remaining stake in 2015 for another $33 million. The company currently has two manufacturing facilities for SDFs- one in Salisbury, Maryland in the US and the other located in Roorkee, Uttarakhand, India. The two sites collectively have an annual capacity of producing over 3.5 billion doses. The company has planned further capacity expansion at Roorkee facility, and increase SDF capacity by 1 billion doses and expand lines for manufacturing novel drugs.

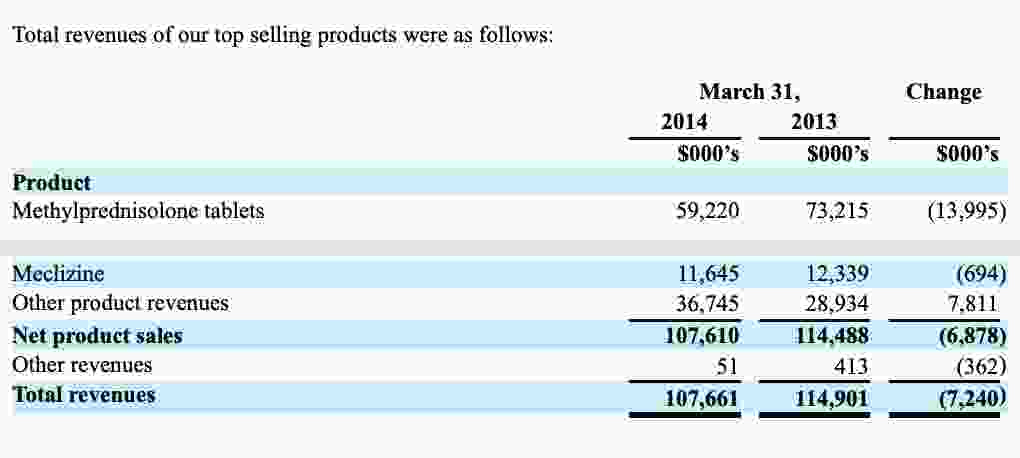

While Jubilant does not disclose product specific sale numbers, prior SEC filings from Cadista Holding, shows their dependence on two products, namely Methylprednisolone and Meclizine for majority of their sales as of 31st March 2014.

These filings also point at the high margins that Jubilant made from the SDF segment. Cadista Holdings according to their 2014 10-K, reported an EBITDA of 44%, down from 58% in the previous year.

Though it would be fair to say that the margins have gone down a fair bit since then, with increased competition in the generic market. Moreover, the consolidation on the customer side, has led to more bargaining power for the customers and put pricing pressure on the manufacturers. Jubilant Pharma reported in FY18, that in the generics segment, top 3 customers accounted for 78% of the their revenues, which was 49% in 2014.

In FY20, Jubilant Pharma (through its subsidiary Jubilant Generics) bought the Indian Branded Pharma business from JLL (parent company) for Rs 128.5 cr. The Indian Branded Pharma business has average sales of around Rs 25cr in the last three years, and an average loss of Rs 17cr ( loss of Rs 9.8cr in FY20). This is a price to sales of more than 4x which quite high in my opinion, with India’s largest pharma companies trading below this.

APIs- Jubilant develops and produces APIs, which are principal ingredients for pharmaceutical formulations, and are also known as bulk drugs. As on 31st March 2020, Jubilant has 44 commercial products and have filed 97 Drug Master Files (DMFs) in the US, 44 CEPs in Europe, 40 DMFs in Canada, 15 Japanese DMFs and 14 filings in Australia. According to Frost & Sullivan, Jubilant is one of the global suppliers based on market share for several key API products, namely, oxcarbazepine (global market share at approximately 30.0%), carbamazepine (global market share at approximately 20.0%), risperidone (global market share at approximately 33.0%), pinaverium (global market share at approximately 20.0%), citalopram (global market share at approximately 18.0%), Donepezil (global market share at approximately 16.0%), and meclizine (global market share at approximately 20.0%). The API segment contributed Rs 640 cr of revenue in FY20, which was 10% of the total Pharma revenue. Unlike SDFs, Jubilant does not have revenue concentrated in a few products, with top 10 products contributing around 10-11% of Revenues. Jubilant manufactures APIs for captive consumption as well, but third-party customers account for more than 80% of their sales. Sartans (angiotensin II receptor blockers) are a key focus area for Jubilant. Hence, the recall of sartan medicines due to detection of carcinogenic impurities in some batches, affected sales in FY20. The company has also had to review and modify manufacturing process which has lead to lower capacity utilisation due to additional quality checks. For the API business, the majority of the competition is from other Indian players, including Ipca Laboratories, Dr. Reddy’s, Aurobindo Laboratories, Lupin Limited, Glenmark Pharmaceuticals and Cipla Limited. Taking Ipca for comparison, they have grown their international API business from $80 million in FY17 to around $130 million in FY20, hence overtaking Jubilant. Jubilant needs to focus on not only new product launches but also geographical expansion.

Jubilant received a Warning Letter at its SDF facility at Roorkee and an OAI (Official Action Indicated) classification at its API facility at Nanjangud from the US FDA due to some problems in their manufacturing process and/or facilities. This has delayed approval for new products from these facilities, but after green light from TGA Australia and Health Canada this issue seems to be resolved.

Jubilant has signed a Licensing Agreement with Gilead, to register, manufacture and sell Gilead’s investigational drug, Remdesivir, a potential therapy for Covid-19. In August 2020, the company launched its Remdesivir product in India and other countries under the brand name “JUBI-R”. The Key starting material (KSM) and API for the product is being manufactured in-house and the manufacturing has been outsourced to a 3rd party (Saptagir Laboratories). The company has capacity of 200,000 doses per month and planning to double that in coming months, as the current quantity has already been placed and there’s demand for more. Jubilant has launched it at a price of Rs 4700 per 100 mg, with Zydus launching the cheapest at Rs 2800 per 100mg.

Contract Manufacturing of Sterile and Non Sterile Products (CMO)- Jubilant got into the CMO business in 2008, by acquiring Hollister-Stier Laboratories for $138.5 million. CMO recorded revenue of Rs 898.7 cr ( or $118.7 million) in FY20, which was 15% of the Pharma revenues. Now, Jubilant has two product segments under our CMO business line: (i) sterile injectables, accounting for approximately 80.0% of CMO revenues is the primary product segment; and (ii) non-sterile products, accounting for the remaining 20.0% of CMO revenues. They offer services for a broad range of sterile injectables, including vial and ampoule liquid fills, freeze-dried (lyophilized) injectables, biologics, suspensions and water for injection diluents. They also offer products that include sterile ointments, creams and liquids and have a growing presence in topical and ophthalmic areas. Services for non-sterile products include semi-solid dosage formulations, including antibiotic ointments, dermatological creams and liquids (syrups and suspensions). Jubilant has an established position in this market and sees this business growing, due to the increased consolidation, with large pharma companies buying CMOs, and reducing their ability to service other customers, hence leading to a demand-supply disequilibrium in the market.

Jubilant has two CMO facilities- in Spokane, Washington, United States and in Kirkland, Montreal, Canada.

The CMO segment faced a setback in 2013 when, the facility in Canada was issued a warning letter by the US FDA. This forced the company to take on remediation activities and shutting down the plant for an extended period, leading to revenue loss and customer drop outs. The company used to have an annual revenue of around $130 million in FY13 and suggested in FY16 they would be back at those levels in “2-3 years” but they have been unable to do that and have averaged around $100 million in the last five years, reaching $120 million in FY20. This recent growth has been due to capex on a new lyophilization line and shifting to 24x7 shifts at the plants. Jubilant has long term relationships with their top customers, with 6 of their top 10 customers having been customers for 10 years or more.

The company recently entered into 4 clinical and commercial supply agreements for Covid-19 treatment and vaccine candidates. These contracts acc. to Jubilant, may contribute additional Rs.230 crore to Rs.450 crore revenue in next 12 to 15-months depending upon product approvals by US FDA.

Allergy Therapy- This segment provides products to the allergy specialty industry with an offer range of different allergenic extracts and standard allergy vaccine mixtures, including insect venom products for the treatment of allergies to insect stings. The Allergy Therapy segment contributed around Rs 408 cr in FY20, which was 7% of the Total Pharma Revenue. The products are distributed to allergists, ear, nose and throat physicians, general physicians and a few hospital-based clinics across North America, under the “Hollister Stier” brand. According to Frost & Sullivan, Jubilant Hollister Stier (JHS) is one of the top three players in the allergenic extract market in the United States with a market share of 17.6%. The allergy therapy products are manufactured at the Spokane Facility. The industry is much more stable (in comparison to generics) and company has managed to grow well in the last five years ( CAGR of 12.5%). Going forward the growth will depend on geographical expansion and new product launches.

Drug Discovery and Development Services - Jubilant Biosys is a wholly owned subsidiary of Jubilant Pharma, which provides drug development services to global pharmaceutical and biotech companies in various biological fields.

Company has done some consolidation in this segment by merging Jubilant Chemsys into Jubilant Biosys at end of FY20. Jubilant Biosys has been a business that has turned around in the last two years, increasing revenue and showing profits as well. From FY11 to FY18, Jubilant Biosys averaged a Revenue of Rs 86cr and Loss after tax of Rs 14cr approx. But in the last two years the company has recorded revenues of Rs 158cr (in FY19) and Rs 143cr (in FY20), at the same time generating profits of Rs 64cr (in FY19) and Rs 36cr (in FY20). The management has suggested that they expect this performance to continue with a healthy order book and strong demand from Bio-tech companies, so much so that they are going to double their research capacity in a couple of years to meet the growing demand.

The research business has seen Jubilant book heavy losses in the last decade-

In FY12, Jubilant had to take a write off the assets of around Rs 150cr , as they were unable to turnaround the loss making Clinsys USA business.

Jubilant Life science Ltd (JLL) had given Jubilant Biosys, loan of Rs 151cr and had to write off the same , along with accrued interest of Rs 35 cr , as the company decided the same was unrecoverable in FY15. Jubilant Biosys had direct promoter ownership of around 31% and rest was owned by the parent company (JLL) through subsidiaries. In order to recover the amount, the company converted the loan into 187,000,000 12% optionally convertible preference shares of Rs 10 each, which were then converted to equity shares, making Jubilant Biosys, a wholly owned subsidiary of JLL.

Moreover in FY20, Jubilant Biosys has contingent liabilities of Rs 104cr , due claims from the Income Tax Appellate Tribunal.

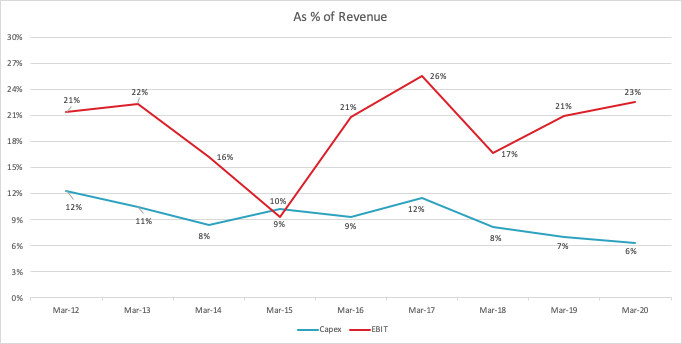

Jubilant Pharma has largely been to maintain its EBIT margin has largely been able to maintain, over the years, with a dip in FY14 and FY15 due to higher costs and lower revenues in Spokane facility due to FDA warning letter. Fall in FY18 relating to acquisition of Triad, and pricing pressure in SDFs and APIs.

The margins are expected to remain in this region for Jubilant Pharma going forward.

While the Capex in absolute terms has increased in the last few years, it has fallen as a % of Revenue. The company was spending around 8.5% of Pharma Revenues in product development, while the absolute amount has remained in that range, Triad’s addition has decreased it as a % of Rev.

Recent capex in Pharma apart from the acquisitions, has been on increasing capacity of SDF facility, spending on a new API plant, and de-bottlenecking in CMO facility and adding new Lyophilization line. The capex in future will be on product development with Jubilant increasing focus on Novel Drugs and as they get into clinical trials.

Jubilant Pharma has long term debt of $400 million and working capital of around $31 million on its Balance Sheet as of March 2020, with a cash balance of around $75 million. Company has $200million of 4.875% Senior Notes maturing in October 2021 (after the company prepaid $100 million in FY20). The rest $200 million of 6% coupon Bonds are repayable in March 2024. The company expects to make these payments from internal accruals.

Jubilant Pharma had taken a zero coupon loan of $60 million from IFC in FY14, this loan was optionally convertible into shares of the Jubilant Pharma upon an IPO, which the management was considering then. In FY19, the management decided against an IPO for Jubilant Pharma and had to redeem this loan from IFC at a premium according to the terms of the deal, making a payment for $135 million. This gives a compounded interest of around 17.6% for JPL. For comparison, the interest cost on dollar loans for JPL has averaged around 5% and 8% for Rupee loans.

JPL has averaged around $140 million in Operating Cash Flows in the last five years, and averaged around $50 million in Capex. Assuming the company has no big acquisition planned in the next five years, JPL should be able to manage its capex and payout their loans without dipping into the debt market.

Overall, Jubilant Pharma has grown at a steady pace and maintained a healthy margin in line with their pharmaceutical peers. But, the growth has not been as impressive once the radiopharmaceutical industry revenue is removed. The company has a variety of products in the SDF and API segments but most have been crowded out and hence put pricing pressure on Jubilant. The company needs to focus on getting into less saturated markets and spend their dollars there. The China de risking- will open up opportunities for Jubilant in APIs and CMO segments, with additional capacity being added to both, and the Covid-19 related treatment should also aid revenues positively in my opinion. With remediation activities in Nanjangud and Roorkee complete, the product approvals from there should start coming in.

The recent appointment of a new CFO - Alok Vaish from FY21 and then him resigning in 6 months, is a point of concern. The details for the resignation are not available at the time of writing this letter. Hopefully, we will get more clarity from the management in the Q2 FY21 earnings conference.

Hi!

If you liked the above letter, consider subscribing to my newsletter ( there must be subscribe button somewhere !!), and follow us on twitter. We will be posting one such article every month. Do leave a comment and share it, letters like ours spread from word of mouth.

Thanks for reading!!