Phoenix Mills Ltd

One of India's largest retail mall developers..

Hi fellow investor,

( Disclosure: I do not own shares of Phoenix Mills Ltd and my views on the topic may be biased. Everything I conclude in the article is solely my opinion based on publicly available information. This should not be taken as financial advice. This is purely for educational purpose.)

Let’s get straight into it.

What is Phoenix Mills?

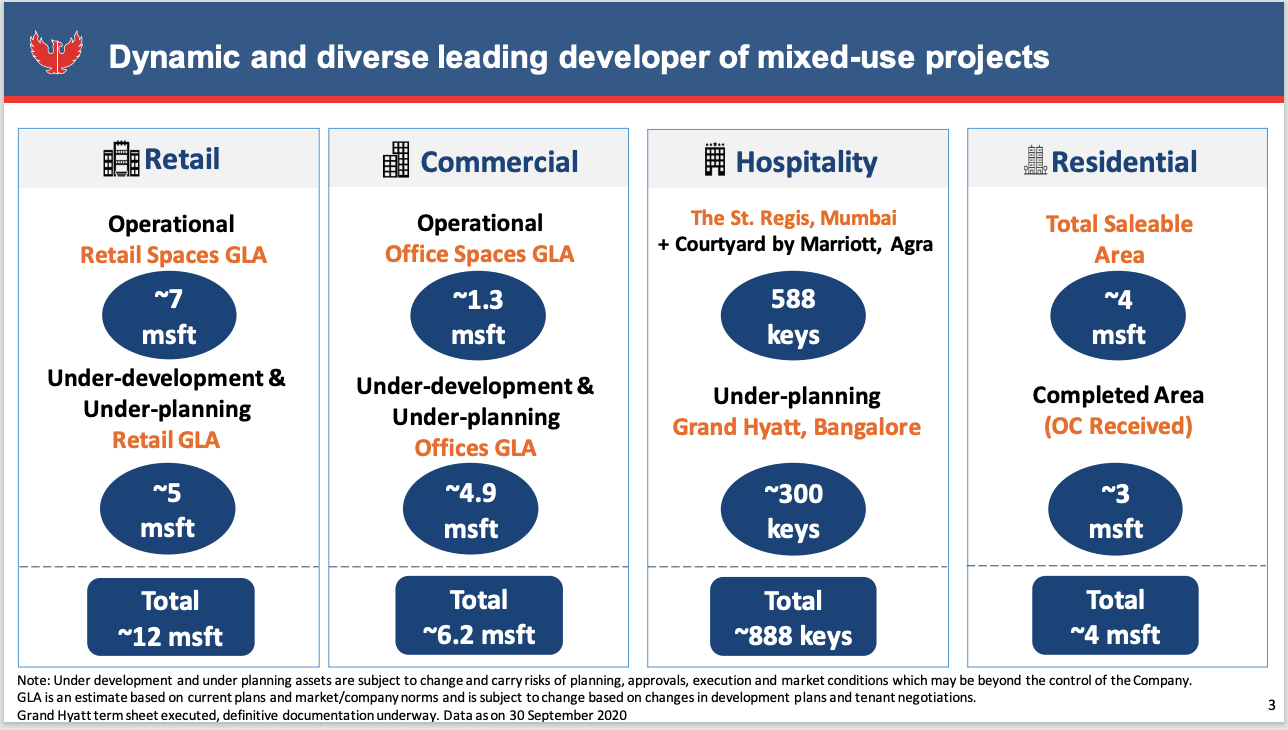

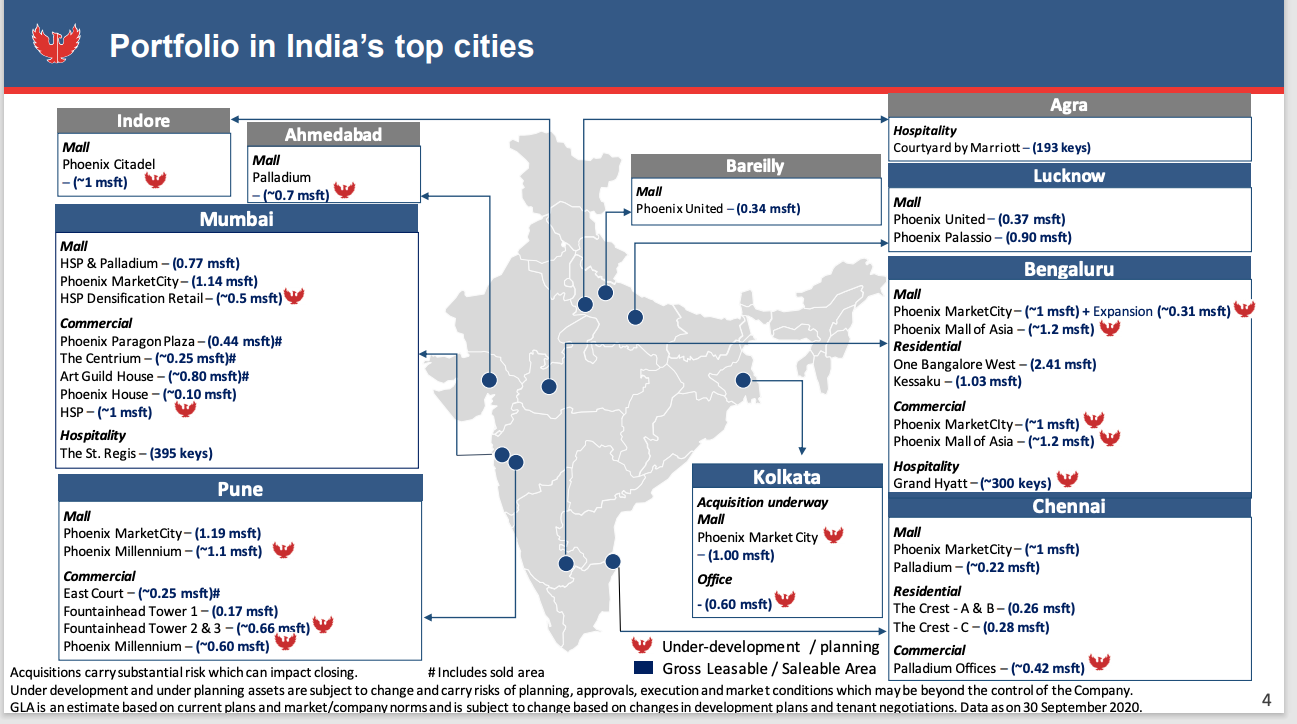

Phoenix Mills Ltd, started off as a cotton textile company in the 1900s, but has in the last decade or so, transitioned into one of India’s largest retail mall developers. The company’s flagship property (it’s first retail mall) is the High Street Phoenix and Palladium Mall in Lower Parel, Mumbai, built on the remnants of the old mill. It’s an iconic property that attracts footfalls of over 20 million per year. The company, lead by its promoter Atul Ruia, has on the back of this developed its own brand of mixed-use assets, that they call the “Phoenix Market City”. The company has currently four PMCs under operation, in Pune, Bangalore, Chennai and Mumbai (Kurla). The Phoenix Market Cities have large retail malls ( of 1 mil. sq. ft or more) as the centre of attraction, and around which they build commercial and residential properties. Phoenix currently has leasable area of around 7 mil sq. ft. across 9 malls in six cities and further 5 mil. sq. ft under development, expected to be operational by 2024. Phoenix in addition to its retail assets, has 1.3 mil sq. ft of leasable commercial assets and saleable residential area of 4 mil sq. ft. The company also has two hotels under operation- St. Regis, Mumbai & Courtyard by Marriott, Agra.

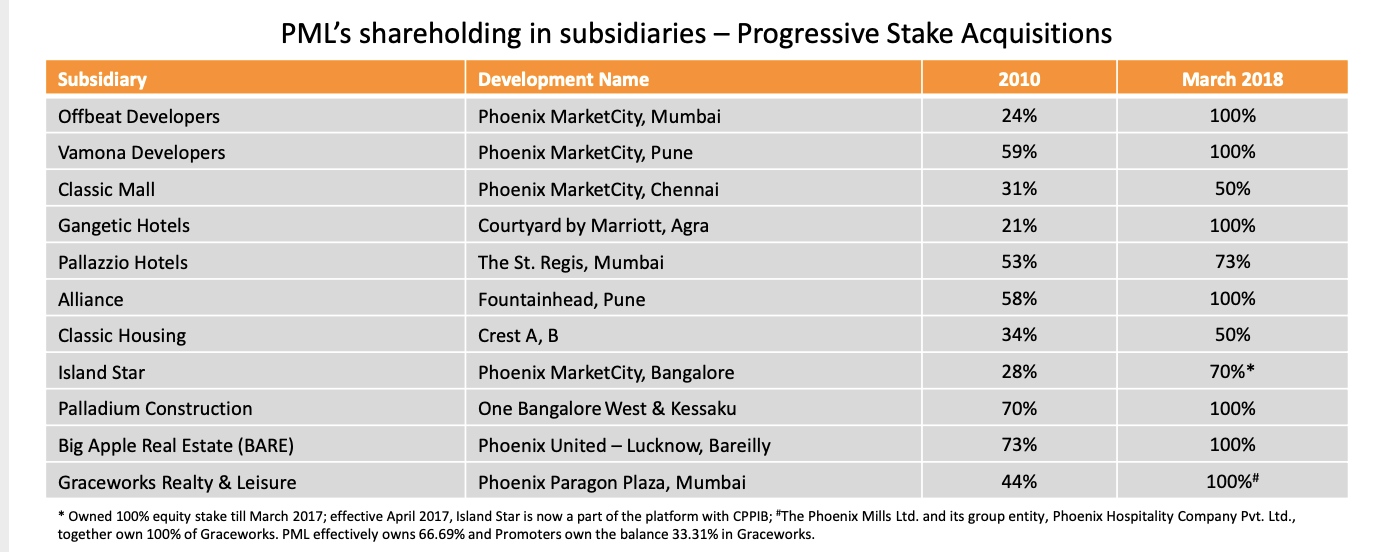

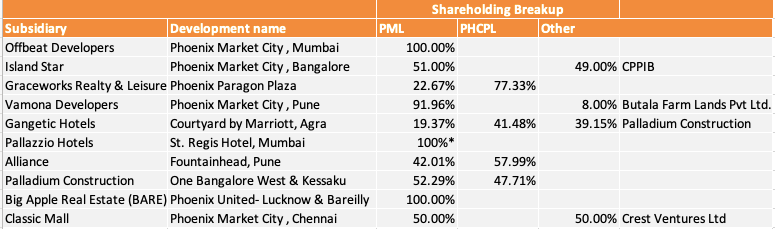

The company operates the HSP & Palladium mall under the standalone entity while the rest of the assets have been developed through SPVs with various other partners. The company has managed to increase their stake in these SPVs over the years, and most are now 100% subsidiaries of PML.

Some of the assets like Palladium Construction, Alliance Spaces, Gangetic Hotels and Graceworks Realty are not really 100% owned by PML, as certain % of these assets are owned by Phoenix Hospitality Company (PHCPL). PML owns 56.92% of PHCPL, while remaining is owned by Ruia International Holding Co. which is a promoter holding company. The break up in shareholding is shown below-

Butala Farm Lands is a 100% owned by PML.

Crest Ventures is a partner in the Chennai PMC and owns the the remaining 50% in Classic Mall and Housing Projects

PML in FY19 sold 49% stake in Island Star to Canadian Pension Plan (CPPIB) for approx. Rs 1600cr. (more on this later)

Pallazzio Hotels is currently 100% owned by PML, but once the Compulsorily Convertible Debentures are converted into equity, PML’s equity interest will fall to 73%, while Avinash Bhosale Infrastructure Ltd (ABIL) will pick up the remaining equity interest.

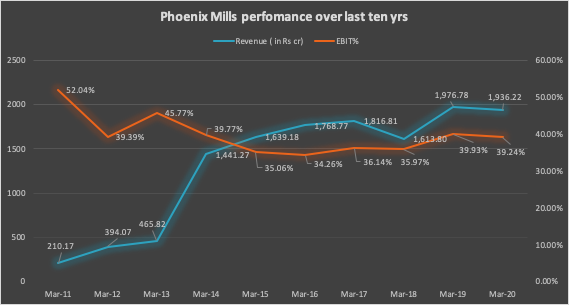

How have they performed in the last ten years?

Phoenix Mills launched the Palladium mall in FY10, and since then have managed to increase their consolidated revenues from Rs 123 cr to Rs 1936 cr in FY20 at a CAGR of 31.7% .

This growth has been possible due to the increase in total leasable area from 1.26 mil. sq. ft. in 2010 to 8.9 mil. sq. ft. in 2020. Rental Income, from commercial and retail properties, contribute around 50% of their overall revenues and are responsible for the consistent EBIT performance, over the last ten yrs.

The rental income has grown from under a Rs 83cr in FY10 to Rs 914cr in FY20 at a CAGR of 27.1%. Retail made up 82% and commercial 18% of the total rental incomes in FY20. The consistent increase has not been just due to addition of new properties but due to the success of these properties allowing the management to increase the rent charged. The company generally signs leases of 3-5 yrs, most retailers have a mixed rental agreements- with a fixed and variable component, all stores pay a minimum guaranteed rent ( fixed ) and if the consumption per sq. ft in the store crosses a certain mark, they also have to pay rental as certain % of their turnover (variable). When the lease agreements expire, the company renegotiates the terms with the retailer, this gives the management the opportunity to increase the rent and also if they feel the consumption from the store not to be satisfactory, look to bring in a different mix of retailers.

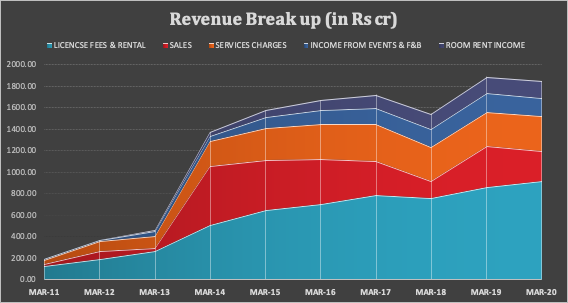

What about the remaining 50% of Revenue, you ask ? Well the mix of the rest keeps changing, Service Charges made up around 18% of revenue in FY20 ( averaging around Rs 320cr each yr), these are the maintenance charges (security, cleaning, electricity, etc.) that the management recovers from the retailers at end of every month in addition to the rentals.

Sales, it’s the revenue the management recognises from sale of residential or commercial properties each year.

In FY20, Sales made up 15% of the consolidated revenues.

Acc. to the Annual Report 2020- “Revenue is recognised at a point in time when the legal title has passed to the customer and the development of the property is completed. The revenue is measured at the transaction price agreed under the contract.”

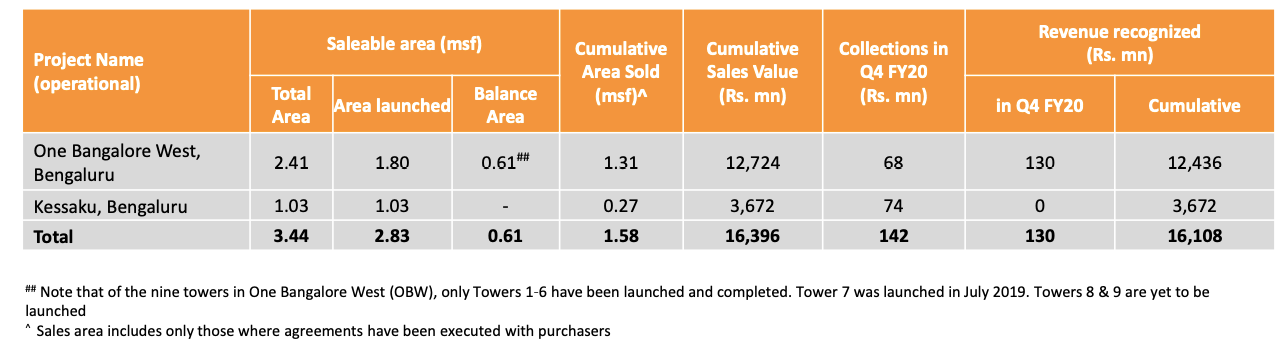

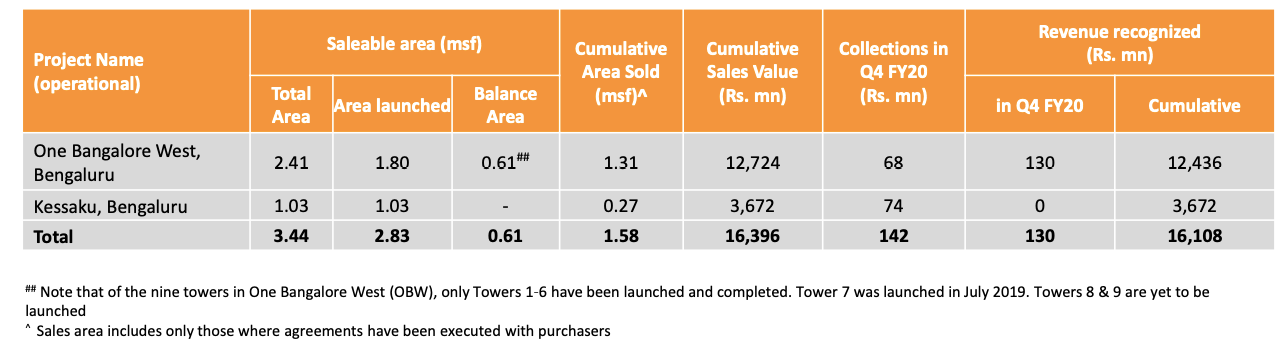

The company has two projects that are consolidated in the revenues- One Bangalore West (OBW) and Kessaku, both located in Malleshwaram, Bangalore. OBW has nine towers of which, 6 are complete and Kessaku is complete as well.

The company till FY20 made cumulative sales of Rs 1639.6 cr, and recognised Rs 1610.8 cr in the financial statements. In addition they have inventory of around Rs 1600cr in the two projects.

Income from F&B and Events made up 9% of the consolidated revenues in FY20. Phoenix through its wholly owned subsidiary Bellona Hospitality, owns and operates 7 F&B outlets across 4 malls in 3 cities. The core brands being Craft, Shizusan Shophouse & Bar and 212 All Good. The majority of this income though comes from the F&B at the St. Regis, Mumbai hotel, which has averaged around Rs 130cr in the last three years.

The income from Rooms, made up the remaining 8% of the revenues in FY20. Phoenix has two hotels under operation, St Regis, Mumbai - which contributed Rs 137cr and Courtyard by Marriott, Agra which contributed Rs 20cr, in room rentals in the last financial year.

So how has Covid-19 affected Phoenix Mills?

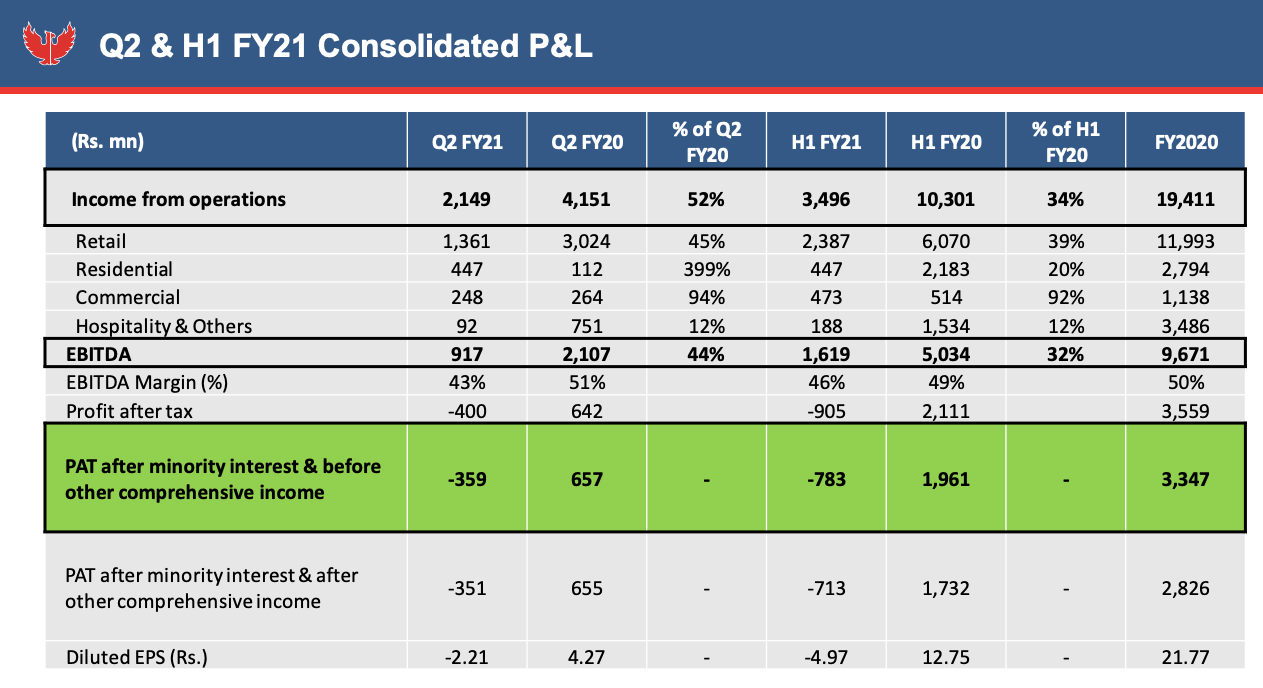

As far as H1 FY21 is concerned the numbers aren’t great, as you would expect as most malls were were closed for the majority of Q1 and when they opened it was under restricted conditions.

The Commercial portfolio, as seen above, has been the least impacted of all the asset classes, the company has even been able to collect 80% of the billed amount.

Hospitality has suffered the most, the company has undertook measure to cut costs, like shutting down restaurants until demand improves, to reduce the cash burn, which is in region of Rs 2-3cr / month , for both hotels combined.

In the retail portfolio, management has negotiated contracts with 90% of the retailers in all malls, giving moratorium on rent payable for the first 3 months, and a rent discount of 50-75% on case to case basis, for limited period, not going beyond FY21, while increasing the revenue sharing percentage. The company has also put in terms, such that, if the consumption exceeds 75%-80% of last yr, the retailer will for that month have to revert back to the FY20 rent agreement.

The company has indicated that, consumption in first week of November reached 85% of last yr, with footfalls averaging 50% of last yr, across all malls. This increase though, could be due to pent-up demand, and multiple festivities falling in the same month. The management still expects to see significant improvement in Q3 and Q4 of FY21, with restaurants and multiplexes also opening up, and expects to end FY21 with 50% of retail rental income of FY20.

In the residential assets, company has seen some demand picking up with cutting of stamp duty and home loans interest rates falling. The company has sold 18 units from July to November 2020, for around Rs 110cr.

The company ended H1 FY21 with Cash and eq of Rs 1850cr, after raising Rs 1080cr through QIP. Company intends to use this cash as buffer till situation improves and then expects to use it as a ‘war chest’ for acquisitions.

Company has gross debt of Rs 4470cr and expects cash outflow of Rs 480 cr for interest and principal repayments in H2 FY21, in addition to that they have capital expenditure plans of around Rs 185cr . With Rs 342 cr in cash inflows in Q2, and situation improving in Q3 and Q4, company should be in a position to meet their cash outflow demands without needing to raise more funds.

How has the retail assets faired in the last ten years?

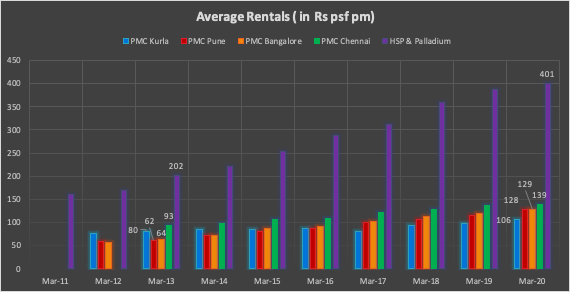

Phoenix Mills has five major retail malls that have matured over the last ten years, while Palladium Mumbai was operational in FY10, PMCs in Kurla, Bangalore and Pune became operational in FY12 and the Chennai PMC became active in FY13. The HSP and Palladium mall has by far been their best performing asset in the last decade.

As seen above, HSP has managed to double the average rental per sq. ft per month from around Rs 200 to Rs 400 in 7 years time. In the same time, the Pune and Bangalore PMCs have managed to do the same, going from around Rs 65 psf pm to close to Rs 130.

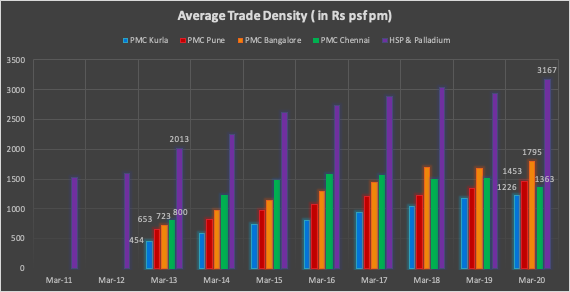

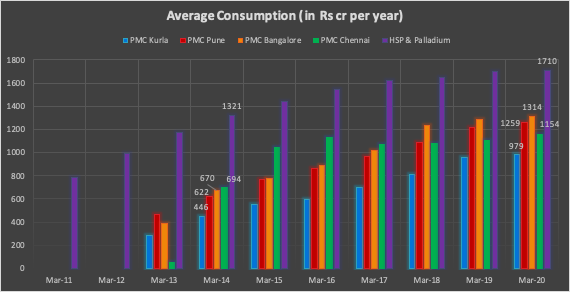

Among the PMCs, Kurla has been the worst performer, while the other three have been neck to neck. Having said that, all the malls have seen consistent improvement in rentals, consumption and trading density through the last decade and are in similar position in which HSP was back in FY12.

It’s visible that due to the slower pickup in mall activity in Kurla, management has been unable to increase the rental incomes there, at the same rate as that of other PMCs, which have managed around 10% rental income increase each yr. Management does believe that the catchment is poorer in comparison to other PMCs, but expected numbers to improve with Monorail, Santa Cruz Link road and Eastern Freeway opening up and increasing the connectivity to the mall.

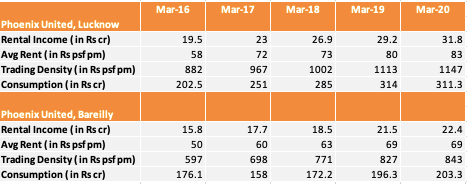

Phoenix Mills also has a couple of smaller malls under the SPV- Big Apple Real Estate (BARE) in Lucknow ( 0.37 msf )and Bareilly ( 0.34 msf) , under the ‘Phoenix United’ brand name.

Are there any other malls currently under development ?

Phoenix launched its second mall in Lucknow in FY20- Phoenix Palassio. It has leasable area of 0.9 mil. sq. ft., its been built in the PMC model and the company has managed to lease out around 85% of the mall. The management believes the malls performance will be similar to that of Pune PMC, as they have similar brand mix. The mall is owned 100% by PML under the SPV- Destiny Hospitality and was under construction when acquired by PML for Rs 453 cr in FY18.

PML has also gone into a 50:50 JV with BSafal Group and acquired 5.16 acres of land in Ahmedabad ( near the Sarkhej–Gandhinagar Highway) to build a luxury mall- Palladium Ahmedabad. The JV has acquired the above land for Rs 230 cr.

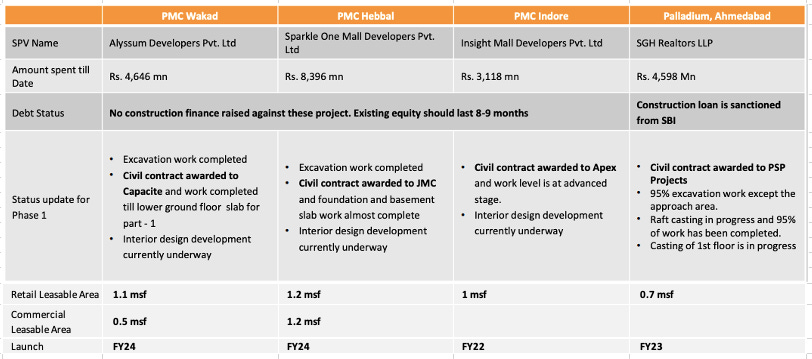

In FY17, Canadian Pension Plan Investment Board ( CPPIB) made an agreement with PML, to invest in two tranches, Rs 1662 cr for 49% stake in Island Star Mall Developers. The funds were to be deployed towards acquiring and developing greenfield/ brownfield assets and to turn them into ‘PMC Models’. PML thus acquired,

A 13 acre land parcel in Wakad, Pune with total development potential of 1.6 mil sq. ft, for Rs 194cr.

Another 13 acre land parcel in Hebbal, Bangalore, with development potential of 1.81 mil sq. ft. for Rs 693 cr.

and they also bought a partly built mall in Indore for Rs 234cr, with 1.1 msf retail leasable area and further development potential of 0.8 msf.

the remaining funds were to be deployed in expanding the Phoenix Market City, Bangalore.

PML announced on Dec 1st, 2020 that, PML and its subsidiaries ( Offbeat Developers, Graceworks Realty and Vamona Developers) have signed a non-binding term sheet with GIC Private limited ( Govt. of Singapore Investment Corporation), for development of a strategic retail-led mixed use platform. PML and subsidiaries will contribute the following retail assets : Phoenix Marketcity Mumbai and Phoenix Marketcity Pune and the following commercial assets: Art Guild House, Phoenix Paragon Plaza and Centrium, Mumbai as a part of the platform. GIC will initially acquire an equity stake of 26% in PML’s subsidiaries, with option to mutually decide to increase that to 35%. The proceeds from the proposed transaction are intended to be utilised as growth capital for further expansion and acquisition of greenfield, brownfield, operational and/or distressed mall opportunities.

So what about the performance of the Residential Portfolio?

Phoenix Mills has three major residential projects that it has launched -

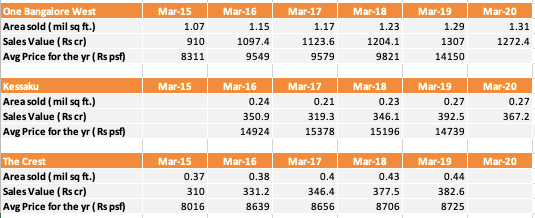

The first residential project they launched was “The Crest” in Velachery, Chennai. It was launched in 2011 and is part of the Chennai PMC. It has three towers (A, B & C) with 0.53 msf of saleable area. The company had sold 0.44 msf till FY19. Only Tower C ( 0.29 msf) sales are consolidated in PML revenues.

They launched “One Bangalore West” in Malleshwaram, Bangalore, in Q2 FY13. It has total saleable area of 2.41 msf off which currently 1.8 msf has been launched. It has 9 towers , 30 floors each, off which Towers 1-6 are built and ready, tower 7 was launched in 2019, tower 8-9 are yet to be launched.

In 2015, the company also launched another residential project in Malleshwaram, Bangalore. “Kessaku” is an ultra luxury residential project with 1.03 msf of saleable area. It is a single tower with 30 floors, the company has managed to complete it in 2019 and have till FY20 sold 0.27 msf.

The residential sales have not been encouraging after the initial launch sales. A large part of blame has been placed on the slowing residential market, and especially low demand for luxury projects. Due to the lack lustre performance, PML has cancelled and converted a few of its residential projects into commercial projects. The Crest had a Tower D with saleable area of 0.42 msf, which has been converted into a commercial project. The Fountainhead in Pune, was built as a residential project with 0.7 msf saleable area but due to lack of interest, had to be converted in commercial as well. There was a residential project planned in the Bangalore PMC as well, which has been cancelled and a commercial project is under planning. The two projects - OBW and Kessaku are under the SPV- Palladium Constructions, and management says they are in no hurry to sell as the asset has very little debt on it. The figures below show the cumulative sales made in each year for respective projects, but please not they are not recognised in the P/L in the same way as revenue isn’t recognised till asset is handed over.

So what are these commercial projects that PML has?

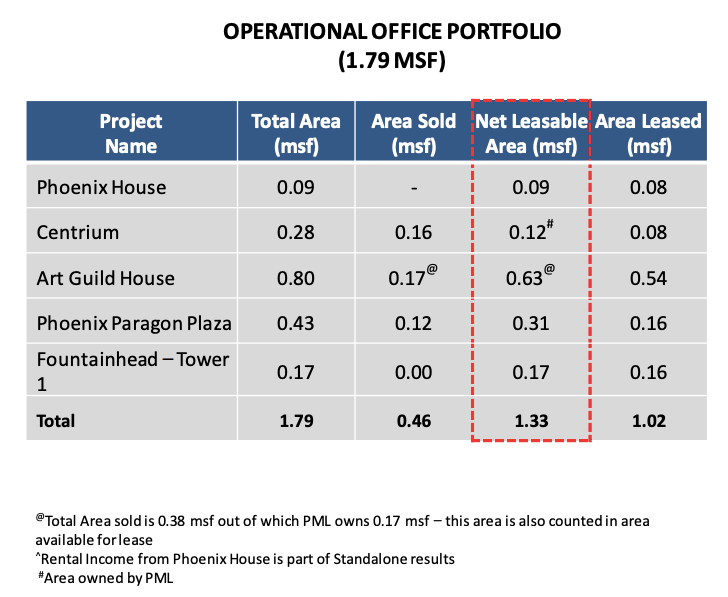

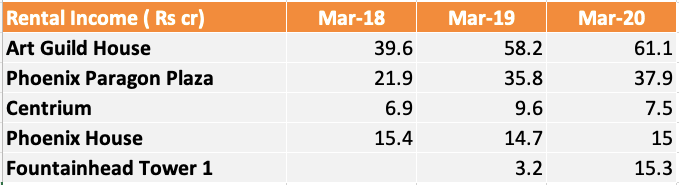

PML has five operational commercial projects-

Phoenix House, located in the HSP complex,

Centrium, Art Guild House, and Phoenix Paragon Plaza are all part of the Phoenix Market City in Kurla, Mumbai

Fountainhead has three towers- Tower 1- 0.17 msf , currently operational, Towers 2 & 3 - 0.66 msf are still under development. All three are part of the Pune PMC.

The commercial projects have a mix of ‘for-lease’ and ‘for-sale’.

The rental income earned by these projects in the last three years-

These commercial projects have not not been home runs for Phoenix by any margin, and they haven’t managed to completely lease out the Kurla commercial properties. Though the response to the Fountainhead project in Pune has been great, as property has been 95% leased out in a year or so after launch.

Talk to me about the Hospitality services?

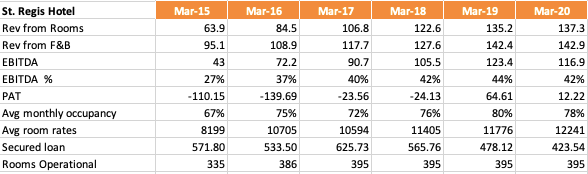

Phoenix Mills launched its first hotel in Dec 2012, after a delay of about a year or so, apparently due to Environment clearance dispute with the SEAC. The hotel was supposed to be operated by Shangri-La , but due to some disputes, the operator left within a year of operations starting. PML finally signed with Starwood Hotels (Marriott) in FY15 and the hotel became operational as St. Regis from September 2015. The hotel is operating under the SPV- Pallazzio Hotels & Leisure Ltd and is part of the HSP complex. Since the new operator has come in, the performance of the hotel has improved considerably and the SPV has turned profitable as well in the last two financial years. The SPV has managed to reduce it debt over the last 2-3 yrs as well.

The SPV has issued a no. of secured and unsecured convertible debentures, to its parent- PML and to the partner in this SPV- ABIL. ABIL will get equity in this asset on conversion of these debentures. ABIL is an infrastructure firm based in Pune, its owner and founder is Avinash Bhosale. It was reported that he was recently questioned in relation to FEMA by the ED.

Courtyard by Marriott, Agra is a different type of hotel to St. Regis, Mumbai. It is more budget oriented and is located 3 km from the Taj Mahal. It is operated under the SPV- Gangetic Hotels, which has been amalgamated into Palladium Constructions. The asset has delivered below results since launch in January 2015.

The hotel has delivered a satisfactory result taking into account its location. Its a five star hotel with great review online - 4.4/5 on Google after over 4000 reviews.

What about competitors?

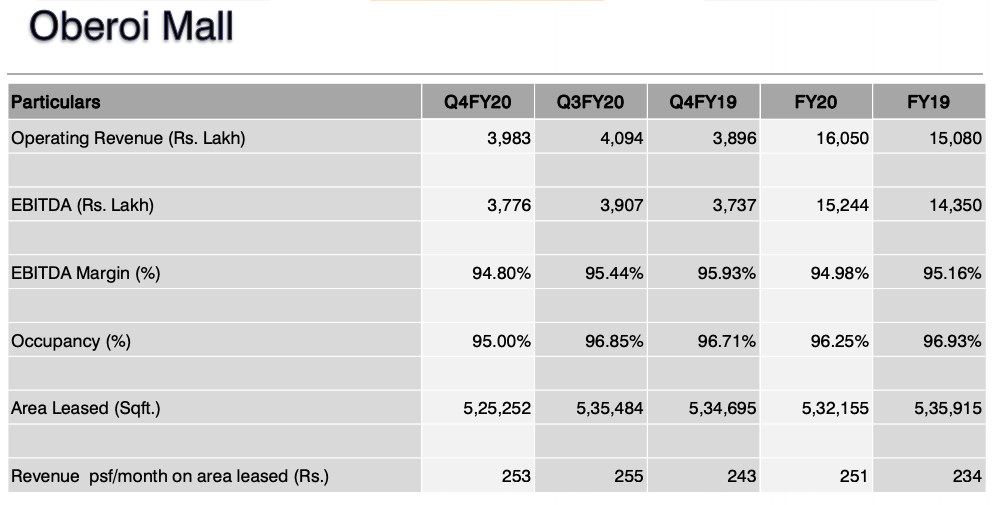

Well the easiest comparison to make would be with listed real estate companies, who operate in similar segments- residential, malls and hospitality. One such company would be Oberoi Realty. They do operate the Oberoi Mall in Goregaon, Mumbai, with a leasable area of 0.53 msf.

Average rentals are more than all malls Phoenix operates with the exception of HSP and Palladium and hence the annual rental income is higher with much lower leasable area. The mall has been in operation since 2008. Though comparison is not fair to malls located in other cities, Mumbai PMC can at least be reasonably compared to this. The Mumbai PMC mall is already in close proximity to R-City Mall, with two more mixed use developments coming up in close range- Maker Maxity and Reliance Convention centre.

Bangalore PMC has UB City to deal with, plus VR Bangalore is a stone throw away from it. But it has a very different catchment area compared to UB City. While VR Bengaluru is right next to it and is definitely a major competitor, the large catchment area is at least currently not affecting Bangalore PMC’s results.

For Chennai PMC located in Velachery, Chennai , there isn’t a mall of that standard located in that area. In Pune while the Inorbit Mall is right across the street from PMC, Viman Nagar and adjoining areas are a large catchment zone and can accommodate two malls.

The two new malls coming up in Hebbal, Bengaluru and Wakad, Pune are both located close to multiple IT parks with no malls of the standard of Phoenix Market city located there. But the interesting proposition for these malls and the new ones coming up in Lucknow and Indore would be whether there is demand for such structures in these locations and hence can the malls earn enough rental incomes to justify the large spend PML has made to build them.

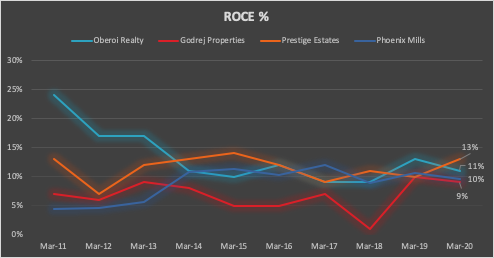

ROCE compared to other Real Estate peers-

What about capital allocation?

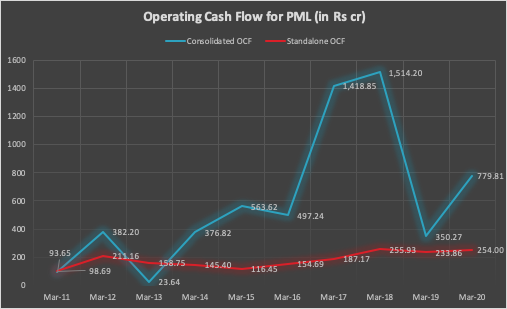

Well by nature of their primary business, which is leasing retail assets, Phoenix generates significant cash each yr. This is evident from the Operating cash flow of standalone entity ( i.e. HSP and Palladium). But the consolidated cash flows have been unpredictable.

The increase in FY17 was due to fall in inventory by about Rs 370cr, fall in capital advances or deposits to related parties & others by about 160cr and fall in receivables of Rs 130cr. In FY18 there was an increase in trade payables due to credit for acquisition, of about Rs 550cr which lead to increase in OCF.

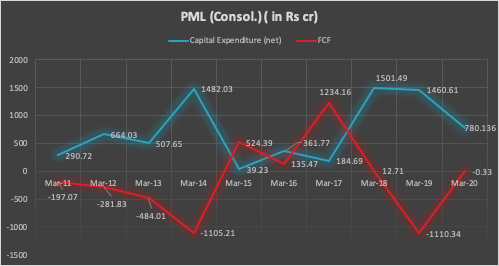

The FCF generation has not been great, as PML has been focussing on developing new assets, whether it be retail, commercial or residential, to increase the top line. This can be seen in the cash outflow each year towards capital expenditure.

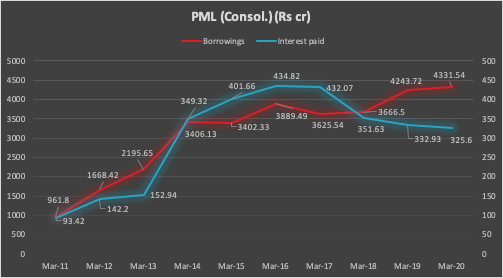

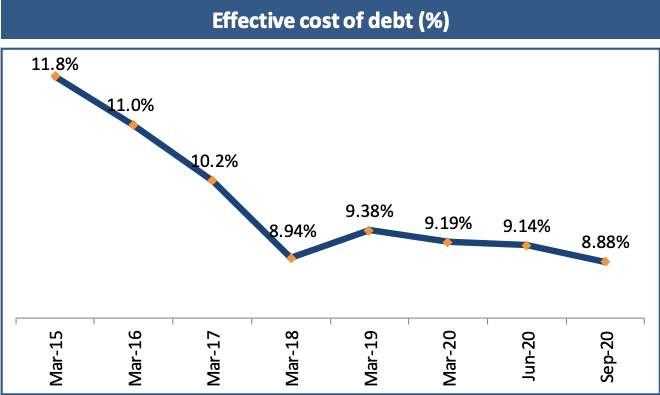

The company thus has had to increase their borrowings to finance these capital expenditures. The interest cost has thus increased with that, but the dependable nature of cash flows from the retail assets, have allowed the firm to raise capital against them. The falling interest rates have helped them as well, currently the lowest rate of borrowing stands at 7.5% and with Rs 2000cr of debt coming up for repricing in Dec’2020 and Jan’2021, company expects to reduce interest cost further.

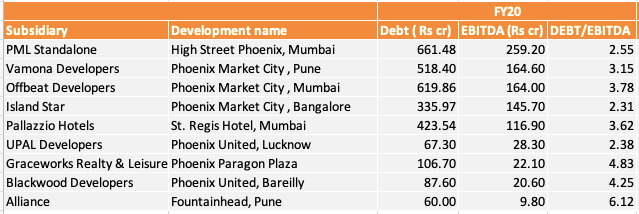

Though the consolidated debt doesn’t give the full picture, as the debt is unevenly divided between all the SPVs.

Most SPVs as can be seen by the Debt to Ebitda ratios are in comfortable position, as most of this debt is long term and majority are Lease Rent Discounting (LRDs), hence are backed by the cash flows the company earns on these assets. Fountainhead still has two towers under construction, so the higher ratio is understandable. Ideally the company should look to reduce these debt no.s further in Graceworks- which has not been able to completely lease out Paragon Plaza ( 0.16 msf off 0.31 msf leasable area).

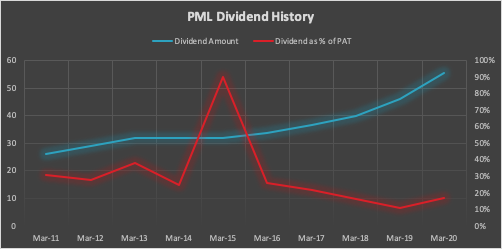

Over the years the company has managed to increase the absolute dividend, but as a % of profit it has been declining.

The one anomaly in the above chart, is due to the reduced PAT in FY15. PML that year had to take write off for Rs 91.25cr ( another 21 cr was written off in FY16), due to impairment of its investment in a JV- Entertainment World Developers Ltd (EWDL). PML had a 40% stake in this company (rest was owned by Manish Kalani) and had invested around Rs 158 cr (not including interest payment due of Rs 14cr). This included 58 cr of equity investment through PML and its subsidiaries and Rs 100cr through fully convertible debentures. PML managed to recover only about Rs 19cr. EWDL was an SPV, developing malls and had three operational malls- 1 in Nanded, Maharashtra and 2 in Indore. They also claimed to be developing another 18 projects. PML later acquired the unfinished Indore mall for the CPPIB platform, for around Rs 235cr in an Asset reconstruction auction.

Anything else to watch out for?

The chairman of Audit Committee- Mr. Amit Dalal and the another member- Mr. Sivaramakrishnan Iyer (a qualified CA), resigned from the Audit Committee , mid year in FY15, though both are still independent directors in the firm. The audit committee also has the promoter himself as a member, which is not ideal.

The key managerial personnel renumeration has increased 5x in the last three years, compared to PAT which has gone up x2. The KMP renumeration was 3% of PAT in FY20 at Rs 10cr, not including the share based compensation.

Final Thoughts!

PML is still in growth mode and is looking to continuously increase that top line, the agreements with CPPIB, GIC, and the QIP shows that the company has the funds to do so as well. The low interest rates in global financial markets have made these investments very lucrative for foreign PE funds. Plus the PE funds are buying directly into the SPV, giving them limited exposure and more control. IF the GIC deal is completed, PML will have sold significant stake in all three PMCs ( Pune , Mumbai and Bangalore) to raise funds for new projects. The new projects will have to deliver similarly to the current PMCs to justify this deal. Moreover, this shows the management doesn’t expect the current PMCs to grow like HSP did from similar position, as they will be facing increased competition from new malls coming up and more importantly E-commerce platforms. If retailers start seeing good sales online, aren’t they likely to reduce existing brick and mortar stores to fewer prime locations! This is where the size and location of the malls will be vitally important. Ideally PML will use some funds from the QIP to reduce the current debt to ease funding requirements coming up for ongoing projects.

Hi!

If you liked the above letter, consider subscribing to my newsletter , and follow us on twitter. We will be posting one such deep dive every month. Do leave a comment and let us know what you think!!

Thanks for reading!!

Close to 50 investors sign petition to EOW mumbai seeking help after investing in Phoenix Mills group